It’s an age-old question: how does car leasing work? It’s quite simple: stump up an initial payment (sometimes referred to as a deposit), choose the best car deal, follow it up with a set of fixed monthly payments, and when the contract is up someone will be round to collect it.

What is a car lease?

Personal Contract Hire (PCH) or in layman’s terms, leasing, is the most hassle-free way of driving a new car, especially if you like changing your wheels every year or two. Road tax and breakdown cover are generally bundled-in.

You don’t own the car, and you never will. And when you give it back, the finance company will expect you to have kept it in good condition. You’re responsible for servicing – although some leasing companies can bundle this into your monthly payments.

And remember to stick to your agreed mileage limit. When you organise the lease, you set a yearly mileage cap. They generally range from 5,000 to 20,000 miles a year. The leasing company will charge you for every mile you go over the agreement. Expect additional fees for any damage to the car, too.

How to lease a car

The process of leasing a car is simple. Broadly you need to figure out what type of car you want, how much you can afford to pay, your mileage limit and your contract length.

The car

This is easily the most fun part. There are hundreds of different new cars on the market, but as a yardstick, you’ll want something that meets your needs as well as your wants. You require something you actually like and want to get in and out of every day, because you’ll be using it for the duration of your contract. Want some help? Check out our car reviews.

Initial payment

This is how much money you put down up front. Remember, this isn’t a deposit as you won’t get this money back. This is a simple payment. Adjusting this changes how much you pay each month. The more you pay here the less you pay monthly.

Price per month

For most people the monthly price is the most important factor when choosing a new car. A quick rule of thumb; it’s recommended that you spend between 10% and 30% of your income on a car. With leasing you’ll never own it – so it can be brought down even more, as low as 5% if you want.

Mileage allowance

Look at your regular driving habits and figure out how many miles you cover in a year. Go too high with your mileage limit and you’re throwing money down the drain. Too low, and you’ll pay for it with additional mileage fees.

Lease term

This is how long the lease lasts for. Generally longer leases cost less per month. But you have to balance this with how often you’d like to change cars.

What happens at the end of a lease?

Once you’ve picked your deal, stumped up the initial payment and paid all of your monthly instalments, your contract is up. Now you return the car and look for a new one. Watch out for the end-of-contract lease charges too.

>> No deposit car leasing: how it works

Benefits and disadvantages of leasing a car

Pros of leasing a car

> Lower monthly payments than Personal Contract Purchase or Hire Purchase

> Lets customers change cars regularly

> Generally the easiest way to drive a brand new car

Cons of leasing a car

> Long-term more expensive than PCP or HP

> No chance to own the car

> Unable to modify the car

> You can’t use Voluntary Termination. But you can still end the agreement early

> You’ll need a good credit score

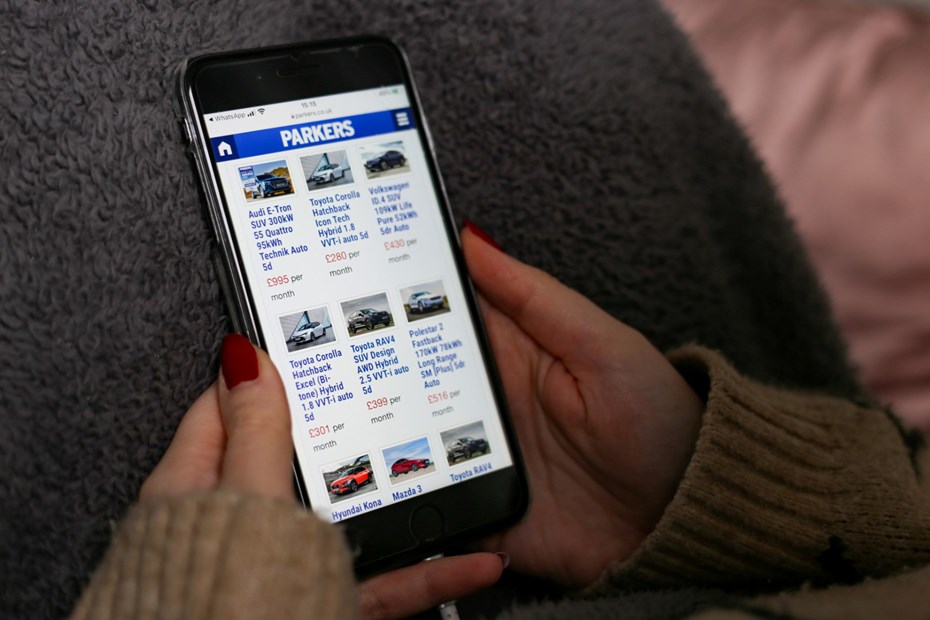

Cost to lease a car

The good news is that there are thousands of leasing deals out there. You’ll struggle to lease a car for £100 per month or less. But upping your monthly cost to £200 per month can land you a practical hatchback, a slinky coupe, or a high-riding SUV. Beyond that the sky’s the limit with leasing costs.

Buying outright, whether that be with a bank loan or via a Personal Contract Purchase (PCP) or Hire Purchase agreement, can work out cheaper over a long-term period because you’ll eventually own the car and will stop having to make payments on it. But that does mean having to keep a car for between six and 10 years to see a saving.

Car leasing options

There are plenty of car leasing options to spend your hard earned money on. Most leasing firms will offer a maintenance package of some description. This bundles car maintenance costs, such as servicing, into your monthly payment.

Other options include the ones on the car itself. Things such as paint colour, parking sensors and cameras can all be specced. One piece of advice – the best leasing deals tend to be in-stock cars. So for the best price you won’t be able to option specific things like paint colour. The good news is that buyers for leasing companies tend to pick sensibly coloured models in popular trim levels as these types of cars are easier to shift.

What credit score do I need?

Generally you’ll need a good-to-excellent credit score in order to lease a car. The reason? From the leasing company’s point of view, those with excellent credit scores have a track record of paying up on time.

Different leasers will have different criteria. A lot of companies will want you to have an ‘excellent’ score, while others might accept merely a good score. You can lease a car with a bad credit score, but it’s a lot trickier. Expect lower prices for people with better credit scores.

Leasing alternatives

The most logical alternative to leasing is buying. We have a separate article on this topic – should you lease or buy a car?

It can be easier to get finance if you’re buying a car rather than leasing, especially if you have a poor credit score.

>> The best new cars for £150 per month

>> The best new cars for £300 per month

>> The best new cars for £400 per month