Van tax is different to car tax. This is good news, as the van road tax rates are much simpler than the car tax rates. It’s also good news as van tax is generally cheaper, whether it is road tax or company van tax – benefit in kind (BIK) tax. If you want to know how to tax everything from a large van to a pickup truck and what it will cost you Parkers is here to help.

Unlike cars, where road tax cost varies with CO2 emissions, under current regulations all petrol and diesel vans are charged the same rate of tax. So whether it’s a small van, a medium van or a large van, the tax cost is the same. The only exception is for electric vans, although there was a major announcement on that front in the 2022 Autumn Statement that will see EV drivers pay VED from 2025 – more on that below.

We also have the updates from the 2023 Autumn Statement, which saw van benefit charges and fuel benefit charges frozen for 2024/2025. Vans and pickups were totally ignored in the 2024 Spring Budget, though, unless you count the announcement that fuel duty is to be frozen. Again.

This lack of update is partly down to the fact that the Treasury had previously confirmed that VED is set to rise in line with the retail price index for the 2024/25 tax year while Benefit in Kind is set to be frozen.

There is also everything you need to know about the pickup tax system. Pickups were going to be treated differently from July 2024, until the government pulled a rapid U-turn. While this means everything remains unchanged for now, it also says that HMRC has its eyes on pickup owners, so there could well be changes in the future.

This page covers:

What counts as a van for tax purposes?

Van tax rates generally apply to all light commercial vehicles (LCVs) up to 3,500kg ‘revenue weight’, including pickup trucks. There are some exceptions, so the surest way to tell if your vehicle qualifies for van road tax is to look at the V5C registration document.

Also known as the logbook, the V5C has a European classification section on it. If this is marked as N1 or N2 then the vehicle counts as an LCV and is taxed as a van.

If it says M1 or M2, however, then it’s a car not a commercial, and subject to car road tax rates instead.

How much does van road tax cost in 2024?

Road tax – officially known as Vehicle Excise Duty or VED – is set at a flat rate for vans.

For the 2023/2024 tax year (which runs from 1 April to the end of March) the cost is £320 for 12 months. The government has confirmed that this will increase in line with the Retail Price Index (RPI) for the 2024/2025 tax year.

VED is collected by the Driver and Vehicle Licensing Agency (DVLA), and you can pay for 12 months or six months at a time, or monthly via Direct Debit. This table compares the costs:

| Payment type | Monthly | Every six months | Every 12 months |

| Outright | n/a | £176 | £320 |

| Direct Debit | £28* | £168 | £320 |

*If you pay by monthly Direct Debit, the annual cost works out at £336, a small extra price to pay for the convenience.

Does the cost of van tax vary?

While van road tax doesn’t have separate bands like car road tax does, van tax does vary depending on the age of the van, and on particularly old vans it’s also different depending on the size of the engine.

Current road tax cost for vans, applies to all models registered from 1 March 2001 excluding exceptions below:

| Road tax (VED) cost | Tax Class |

| £290 | TC39 |

Road tax cost for Euro 4 vans registered between 1 March 2003 and 31 December 2006:

| Road tax (VED) cost | Tax Class |

| £140 | TC36 |

Road tax cost for Euro 5 vans registered between 1 January 2009 and 31 December 2010:

| Road tax (VED) cost | Tax Class |

| £140 | TC36 |

Road tax cost for vans registered before 1 March 2001 up to 1,549cc engine size:

| Road tax (VED) cost | Tax Class |

| £180 | TC11 |

Road tax cost for vans registered before 1 March 2001 with larger than 1,549cc engine size:

| Road tax (VED) cost | Tax Class |

| £295 | TC11 |

As these tables show, Euro 4 and Euro 5 emissions standards have created low road tax vans at times – and these still have cheaper van tax today, even though more modern Euro 6 vans are even cleaner.

Similarly, current small van road tax costs the same as large van road tax, though some vans registered before March 2001 may have lower tax due to having a smaller engine.

But whether it’s a Vauxhall Vivaro or a Vauxhall Astra van, a Ford Transit or a Ford Transit Custom, if they fall into the same tax class they cost the same in van VED.

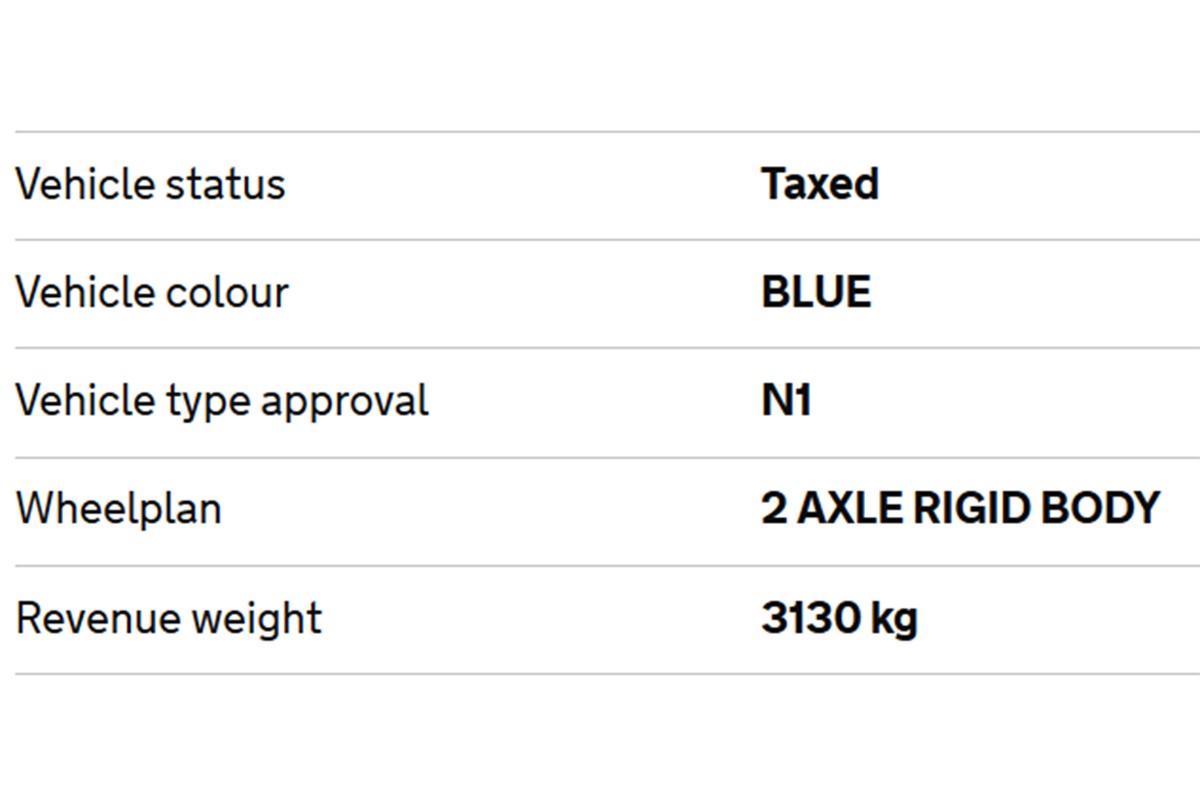

Is my van taxed?

There’s a UK government website that easily allows you to check if your van is taxed – all you need is the van’s registration number (number plate):

You can ask Amazon Alexa or the Google Assistant to find out your vehicle’s tax status as well.

Remember, road tax is no longer transferred between owners, so when buying a used van you’ll have to get it taxed before you drive it, just as you have to arrange insurance.

Any vehicle that uses the public roads must have valid tax, insurance and MOT.

That government webpage can also tell you exactly how much your van tax will cost – but for that you’ll need the V5C registration document as well as the number plate.

How to pay van tax

You can tax your van by visiting the Post Office or telephoning the DVLA on 0300 790 6802, or you can tax your van online via the UK government Tax Your Vehicle webpage:

To pay online or by phone you will need a debit card or credit card. At the Post Office you can also pay by cash, cheque, or postal order.

You’ll also need one of the following official documents:

- A recent reminder letter (known as the V11) or ‘last chance’ warning letter from the DVLA

- The vehicle logbook (V5C registration document) – which must be in your name

- Green ‘new keeper’ slip from the previous logbook if you’ve just bought the vehicle

If you’re taxing at the Post Office but can’t find your V5C, you can also use a V62 form (the application form for a new V5C logbook).

If the vehicle is registered at a Northern Ireland address, you will also have to provide proof of insurance; for the rest of the UK this is now digitized.

MOT records are also digitized, but although you won’t have to show an MOT certificate, the vehicle will need to have a valid MOT for the date the tax first starts.

Van benefit-in-kind tax

Benefit-in-kind (BIK) is the tax you pay on something that’s provided by your work but also a benefit to you.

BIK is collected by HM Revenue and Customs (HMRC) rather than the DVLA.

Company cars are the best-known example, but there is also company van tax, officially known as the Van Benefit Charge.

How is van benefit tax calculated?

As with road tax, BIK rates are much simpler for vans than cars.

All company vans are charged BIK at the same fixed or flat rate: the 2023/2024 van BIK rate is £3,960. This is an increase of £360 over the previous year, and has gone up in line with the consumer price index. The government confirmed in the 2023 Autumn Statement that this would be frozen at the same rate for the 2024/25 tax year.

This means:

- If you’re a 20% taxpayer, van BIK is £792 per year – £66 per month

- If you’re a 40% taxpayer, van BIK is £1,584 per year – £132 per month

Whether you pay 20% or 40% depends on how much you earn.

Either way, that’s a lot less than almost all cars cost.

Do I need to pay BIK on my van?

Because BIK is a tax on benefits, you only need to pay BIK on a van if it’s a benefit to you – which means if you’re allowed to use if for ‘private journeys’ rather than just ‘business journeys’.

If you only use the company van to go to and from places of work, that’s ‘business use’. But if you take it to the supermarket to do your weekly shopping or go away on holiday in the company van, then that’s ‘private use’, and you will have to pay BIK.

‘Insignificant’ private journeys are allowed within business use rules. Examples include a ‘slight detour’ to buy a newspaper on the way to work or taking a pool van home for the night if you have an early working start in the morning.

Can I avoid paying BIK on a van?

You can avoid paying BIK for private use of a company van if you pay your employer for the privilege of using the van privately.

Also, one-off trips – such as taking stuff to the local public recycling centre – are exempt from the private use rule.

And if you do have a company van but aren’t able to use it for more than 30 days in a row, this also means you shouldn’t have to pay BIK on it.

Another option would be to lobby your employer for an electric van. On which more below.

Van Fuel Benefit Charge

If you claim the cost of fuel from your employer for business use only that’s not a benefit – but if you claim the cost of fuel for private use then that is a benefit, and you’ll have to pay the Van Fuel Benefit Charge.

The 2023/2024 Van Fuel Benefit Charge rate is £757. As this is the benefit rate:

- 20% taxpayers have to pay £151.40 – around £12.62 per month

- 40% taxpayers have to pay £302.0 – around £25.23 per month

Not only is this cheaper than the fuel benefit charge for company cars, the amount can be shared between employees who use the same van. In the 2023 Autumn Statement, the government confirmed that the rates will remain the same for the 2024/2025 tax year.

What’s more, it will also be reduced if:

- You can’t use the van for more than 30 days in a row

- The private-use fuel provision is taken away by your employer during the year

- If you pay your employer back for the cost of the private-use fuel

Keep records of every journey

The best way to ensure you’re not being unfairly taxed is for you and your employer to keep records of every journey.

An increasing number of light commercial vehicles are available with built-in connectivity that aims to make this easier.

What’s the tax on electric vans?

The UK government has historically been keen to encourage businesses to switch to electric vans, which has meant that they have attracted zero VED and BIK rates. Up until 1 April 2025, the following rates apply:

- Electric van road tax is £0

- Electric van BIK is £0

Literally zero.

However, this will all change with the start of the new tax year in 2025, when the government has elected to bring electric vans into line with petrol and diesels. This means that you will pay the same rate regardless of what you use to power your vehicle. The rate is £320 as of 2023, but this will rise in the meantime.

What is not yet clear is whether this will be backdated – electric cars bought in the years leading up to 2025 will also move onto the new system, but the government has not yet said whether existing vans will move over as well.

There’s also no Van Fuel Benefit Charge on electric vans as, to quote the government’s official documentation, ‘electricity is not a fuel’. This is not set to change as a result of the 2022 Autumn Statement, as the government has simply said it will rise in line with the consumer price index.

Pickup tax rates

For many years, pickup trucks have been taxed at the same flat rates as vans.

This means:

- Pickup road tax is £320 for 2023/2024

- Pickup benefit-in-kind is £66 per month at the 20% BIK rate or £132 per month at 40% BIK rate

There are exceptions to this for double-cab pickups that can’t carry a 1,000kg payload (or 1,040kg if fitted with a hardtop over the load area); examples include some early versions of the Volkswagen Amarok and the present Ford Ranger Raptor.

Annoyingly, the DVLA and HMRC take a different view on these vehicles. So while the Ranger Raptor (for instance) meets the DVLA’s standards for flat-rate van road tax based on its N1 European classification, it doesn’t meet HMRC’s standards for flat-rate van BIK because of its 652kg payload.

This means BIK on the Ranger Raptor is charged at company car rates – and thanks to its high P11D value this means a bill of around £720 per month for 40% rate payers.

For the same reason, you can’t claim the VAT back on a Raptor and you have to pay the fuel benefit charge at car rates as well. A triple whammy.

All this was due to change as of 1 July 2024, at which point all double-cab pickups were going to be treated as cars. HMRC decided that the loophole needed closing and that most trucks are being used as vehicles for carrying people rather than as working vehicles. However, panic not, as the lawmakers decided to listen to the industry and dropped the plans only a week after announcing them.

While you might rightly ask if they could have asked a few questions before worrying everyone, it is at least good news that they listened in the end.

Other exceptions to the usual van tax rates

Other types of van that cause tax confusion include car-derived vans, commercial 4x4s and – especially – vans with more than one row of seats, such as double-cab vans, combi vans, kombi vans and crew vans.

Again, it’s easy to check the road tax cost of these using the European classification on the V5C logbook – N1 or N2 type-approval means they count as a commercial vehicle for VED purposes while M1 or M2 means they’re classed as a car.

Things get trickier when it comes to BIK, especially for vans with multiple rows of seats.

To meet the definition of a van HMRC uses to decide benefit-in-kind, the vehicle has to be a ‘goods vehicle’ – which means ‘a vehicle of construction primarily suited for the conveyance of goods or burden.’

Car-derived vans (CDVs) and commercial 4x4s should be fine with this because they only have a single row of seating and the rest of the vehicle interior converted for carrying goods and appropriate bodywork. For example, the current Ford Fiesta Van and Toyota Land Cruiser Commercial do qualify for van BIK rates.

The problem for panel vans with more than one row of seating is that they have effectively switched from being goods vehicles to passenger vehicles.

A high-profile Court of Appeal ruling in August 2020 confirmed as much, and has made the van status of all crew and combi models very much in doubt as far as the HMRC is confirmed.

Some are continuing to argue that as long as the van has only two rows of seating and maintains a payload rating of over 1,000kg then it’s still primarily a goods vehicle under the same ‘dual-purpose’ rules that double-cab pickups use.

But given HMRC’s appetite for court action relating to the misclassification of these vehicles you’re better off playing it safe and treating them as a car as far as BIK is concerned.

Van tax FAQs

Our answers to some of the most frequently asked questions about van tax.

How to cancel van road tax

If you need to cancel your van tax, you must contact the DVLA by phone, email or even letter. The only exception to this is if you want to register the vehicle as ‘off the road’ using a Statutory Off Road Notification (SORN); this can be done in moments online.

You will get a refund on any payment that goes beyond the date of cancellation – such as the remainder of a Direct Debit or the rest of a six- or 12-month term. Depending on how you paid, the refund can take up to eight weeks.

The government lists only the following as reasons you might want to cancel your road tax on your van:

- You sold the van or transferred ownership to someone else

- You’ve taken it off road – using a SORN

- It’s been written-off by your insurance company

- It’s been scrapped – at a vehicle scrap yard

- It’s been stolen – slightly different process but you can still get a refund

- It’s been exported out of the UK

- If it’s been registered as exempt from tax

To quote the government: ‘There is no other way to cancel your vehicle tax.

What happens if you don’t pay your van road tax?

Fail to renew your van road tax on time, and you’ll get an automatic £80 fine from the DVLA – though this is halved to £40 if you pay within 28 days. Ignore this and you may end up in court, where the maximum fine is £1,000 or five times the value of the tax you haven’t paid.

If the DVLA sees your van parked on the road without tax it may be clamped, and you’ll pay a minimum £100 release fee, plus a (refundable) ‘surety deposit’ of upwards of £160 if you can’t prove it has now been taxed.

You can also be fined if the vehicle is seen off the road without tax or SORN status – and you can be fined if you have declared it SORN but left it parked on the public road.

If the police catch you driving a van without tax you’re committing a legal offence and will be subject to a fixed penalty notice (FPN) payable on the spot. This could be as much as £1,000. Police use automatic number plate recognition (ANPR) cameras to detect this kind of thing.

Worst case scenario, your van could even be seized and impounded.

Are there any vans with £30 road tax?

Short answer: no.

Slightly longer answer: there have been some passenger versions of particularly small vans that have qualified for the £30 road tax band in the past, but that’s because these have actually had the legal status of cars rather than vans.

What is a pool van?

A pool van is a van that’s available for use by more than one employee, provided because it’s necessary for the job, and not kept at or near an employee’s home (unless needed early the next day).

If your work only gives you access to a pool van then you shouldn’t be paying BIK.

If it’s a company van that several employees regularly use for private journeys and keep at their homes overnight, it may not count as a pool van. However, in this instance, the BIK cost would be divided between each of the employees that has access to the vehicle, reducing the individual cost accordingly.

What is van revenue weight?

To qualify for light commercial vehicle road tax, your van must have a maximum revenue weight of no more than 3,500kg (3.5 tonnes). Revenue weight is the same as gross vehicle weight (GVW), maximum authorised mass (MAM), permissible maximum weight and maximum laden weight – which are all terms the government uses for the same thing: the total legally allowed weight of the vehicle and everything inside it, including the people.

Is a light goods vehicle a van?

Light goods vehicle is indeed another term for light commercial vehicle, and is used in some UK government communications about van tax classes. TC39 and TC36 tax codes/bands are often described as relating to light good vehicles, for example.

Do I need to tax my electric van?

You do still need apply to the DVLA for road tax for an electric van even though there’s no cost – otherwise you’ll invalidate your insurance and may get pulled over by the police for driving an untaxed vehicle.

This is because the road tax process is used to track the number of vehicles on the road as well as for revenue purposes.

How can I find out my vehicle’s European classification?

The European classification – N1 or N2 for commercial vehicles, M1 or M2 for cars – can be found on your V5C registration document, also known as the logbook.

However, if you need to know and don’t have the V5C to hand, you can also find out via the UK government’s road tax checker website: https://www.gov.uk/check-vehicle-tax. Once you’ve entered the number plate and confirmed the vehicle make and colour, you’ll find it listed as ‘Vehicle type approval’.