Halal, or Islamic car finance allows Muslims to obtain modern financing while still following Sharia Law, the moral codes set out by the Quran.

Islamic car finance is popular because it allows strict Muslims to divide the cost of a car into monthly payments while still following Islamic law. Halal car finance is necessary because according to Islam, interest (riba) is forbidden (haram).

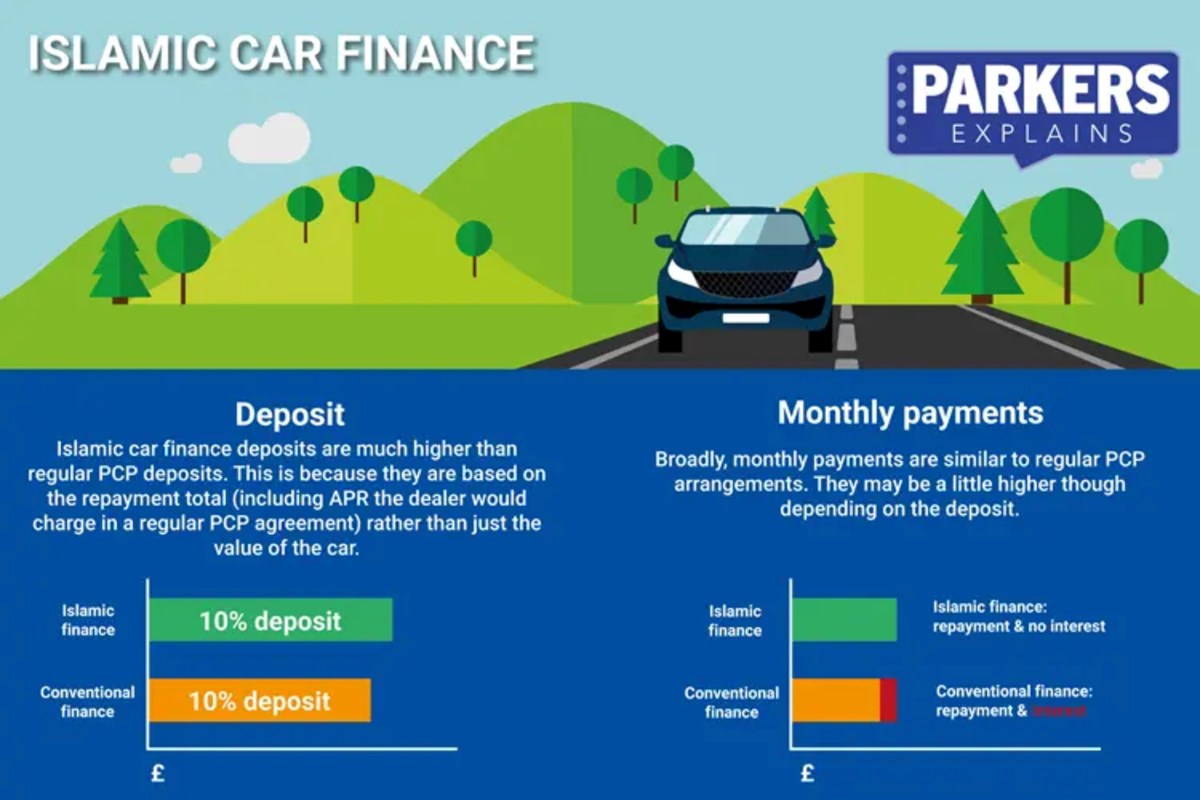

There are pros and cons to it and it isn’t just an easy way to secure an interest free car finance deal. The amount borrowed is essentially the price of the car, plus any interest a seller would charge to non-Muslim buyers.

How does Islamic car finance work?

There are several strands of Islamic finance, but it generally works on the basics of a personal loan, and is actually quite simple.

Instead of the seller making money by charging interest, they simply increase the price to cover the money they would have made by adding an interest rate. Because there is no interest rate added, it’s Sharia compliant.

Deposit rates on Islamic car finance are generally much higher than traditional forms of car lending because they’re based on the overall repayment you make, rather than just the car.

This works differently to conventional car finance options. These typically charge an interest rate – a percentage charged on the total amount you borrow or save, which is typically paid for monthly.

Most car manufacturers don’t offer Islamic car finance specifically, but there are a number of companies that specialise in it. Banks such as Al Rayan and Lloyds TSB also provide Islamic bank accounts.

Halal car finance example

If you bought a car from a dealer for £10,000 on a Hire Purchase agreement with a 5% APR rate, you would pay in total £10,500 over the course of the agreement (assuming for ease that the agreement is over 12 months). £10,000 for the car, and £500 in interest.

Ford Fiesta Hire Purchase agreement

Price: £10,000

APR: 5%

Contract length: 12 months

Total cost to buy car (including interest) £10,500

With an Islamic agreement, the dealer would pre-load that £500 worth of interest onto the price of the car. So you would pay £10,500 (spread over a set of fixed payments) for the car, not £10,000.

Ford Fiesta Halal car finance

Price: £10,500

APR: 0%

Contract length: 12 months

Total cost to buy car: £10,500

Islamic PCP finance

PCP (Personal Contract Purchase) contracts usually require a deposit (although there are no deposit deals out there) which is followed by a set number of monthly payments. Should the customer choose, they can buy the car for a pre-agreed sum at the end of the contract term or simply hand it back

PCP finance agreements are generally unavailable with Islamic car finance because interest is added.

Islamic HP finance

HP (Hire Purchase) spreads the car’s cost across a deposit and a number of monthly payments. Once you’ve paid all of the monthly instalments, you own the car with nothing left to pay.

Traditional Hire Purchase agreements aren’t technically available in conjunction with Islamic finance because interest is added to your monthly payments.

Leasing as an alternative

Leasing (also known as Personal Contract Leasing or PCH) is an elegant solution for people following Sharia Law because it negates interest costs. You’re not charged interest when you lease a car, you simply rent it. Therefore it’s Islamic compliant.

Leasing monthly payments are usually lower than Hire Purchase or Personal Contract Purchase payments too. But there’s no option to buy the car at the end of the agreement, so you’ll never own it.

>> Search for car leasing deals

Just so you know, we may receive a commission or other compensation from the links on this website - read why you should trust us.